{kind=link}

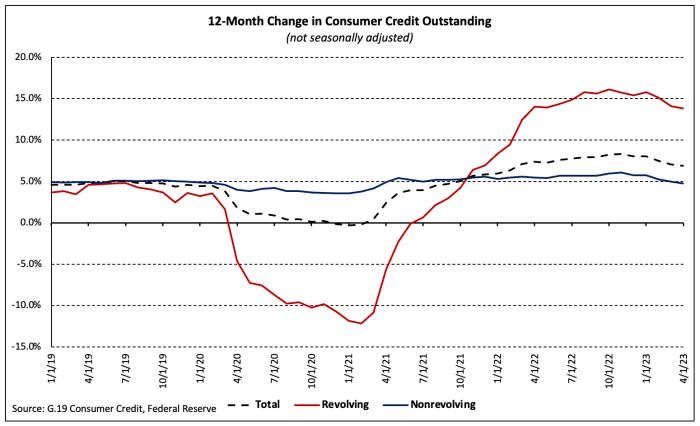

Client credit score excellent grew at a seasonal adjusted annual fee of 5.7% in April 2023 per the Federal Reserve’s newest G.19 Client Credit score report, as revolving and nonrevolving debt grew at 13.1% and three.2%, respectively (SAAR). Complete client credit score excellent stands at $4.8 trillion (not seasonally adjusted), with $1.2 trillion in revolving debt and $3.6 trillion in non-revolving debt (NSA).

The full steadiness of client credit score excellent grew 6.9% over the 12 months ending April 2023 (NSA). Revolving debt grew 13.8% over the interval, almost 3 times the expansion in nonrevolving debt (4.8%).

The 12-month progress fee of revolving debt exceeded 10.0% in March 2022 and has not fallen beneath that mark since. The final time progress exceeded 10.0% was from November 2000 by June 2001, a interval throughout which unemployment started to rise and the 2001 recession started.

Revolving and nonrevolving debt accounted for twenty-four.7% and 75.3% of complete client debt, respectively. Revolving client credit score as a share of the overall fell to 21.8% in April 2021—the smallest share since 1986. At 24.7%, the share is roughly equal to the 10-year common of 25.1%. Between April 2022 and April 2023, revolving client credit score excellent as a share of the overall elevated 1.5 share factors.

Associated